- Prologue

- What is monetary policy?

- Quantitative Tools

- Monetary Policy: limitations

- Qualitative Tools

- Monetary policy tools: Quantiative vs Qualitative

- Appendix

- Mock Questions

Prologue

- Next article is about RBI appointed Urjit Patel Committee on Monetary policy framework.

- But before dwelling into that, we must recap the basic concepts of what is monetary policy: its tools and limitations. Otherwise Urjit won’t make much sense.

- Hence in a way, this whole article is a prologue to next article.

Why RBI and Why Monetary policy?

Initially people used barter system for trading. But the barter system had many problems (click me). Therefore, people switched to money system.

- Financial intermediates = middlemen who help in the circular flow of money between households and business firms.

- There are two types of financial intermediaries: banking institution and non-banking financial institutions.

- RBI controls (all) banks and (some) non-banking financial institutions.

- RBI’s main job is to control Money supply in this game, and thereby fight inflation and deflation.

- Inflation = price rise = bad for economy, you know that by common sense.

But Deflation = price decrease = we can buy things at a lower price. Isn’t that good? Why is deflation bad for economy?

- Ans. Every business has ‘fixed cost of production’ say minimum light bill, phone bill, office rent, staff salary etc. So, if prices keep falling and falling (say of Nano car), then car marker will suffer losses. He has no motivation to expand business. He wants to cut down his production costs, by firing some of the employees= less new jobs created= unemployment = social unrest.

- If prices of everything fall- then custom duty, VAT, excise duty, service tax- their collection will also decrease. Then government has less money to spend on education, healthcare, social sector, defense, law and order = poverty, disease, crime.

by the way

| TERM | meaning | Does RBI want it? |

|---|---|---|

| DEFLATION | fall in the prices (and fall IN employment.) | No. |

| DISINFLATION | Fall in the prices but without causing unemployment. | yes (while fighting inflation) |

| STAGFLATION | stagnation + inflation

|

No |

| REFLATION | policy to stop the fall in price levels, but without causing rise in the price levels (inflation). | yes |

What is monetary policy?

- Policy made by the central bank.

- To control money supply in the economy. (and thereby fight both inflation and deflation).

RBI implements monetary policy using certain tools. Two types

| quantitative tool | qualitative tools |

|---|---|

| Let’s start from here. |

Quantitative Tools

#1: Reserve Ratios (SLR and CRR)

| SLR | A Bank has to set aside this much money into gold or RBI approved securities. | 23% |

| CRR | A Bank has to set aside this much as reserve. Bank cannot lend it to anyone. Bank earns no interest rate or profit on this. | 4% |

Reserve ratio: SLR, CRR

- Suppose economy is showing inflationary trend. Prices of all goods and services are increasing day by day.

- How can RBI stop it using Reserve ratio as a tool?

- In this case, RBI should RAISE the reserve ratios.

Observe:

| Right now | |

| People deposited total this much money in SBI (net demand & TIME liabilities NDTL) | 100 cr. |

| CRR (4%) [SBI has to keep this much cash aside for reserve] | -4 cr |

| SLR (23%) [SBI has to invest this much money in RBI approved securities] | -23 cr. |

| Money left with SBI | 100-4-23=73 Cores. |

Say RBI raises SRL to 40% and CRR to 15% then?

| Originally | 100 cr |

| SLR 40 | -40 |

| CRR 15 | -15 |

| Money left with SBI | 45 cr. |

You can see, when Rajan has raised reserve ratio, money with SBI is reduced (from 73 crores to just 45 crores.)

What will be its implication?

- Imagine you’re a money lender. You’ve 100 crore rupees and you must make Rs.1 crore profit in a year.

- Obviously, you should lend it @1% interest rate. (because 1% of 100 crore = 1 crore.)

- But what if you’ve only 2 crore rupees, and you still want to make Rs.1 croer profit in a year?

- Now you must lend it @50% interest rate. (because 50% of 2 cores = 1 crore.)

- Observe that as money decreased (from 100 to 2), loan interest rate increased (from 1% to 50%).

Same happens when SBI is left with less money (after RBI increases reserve ratio).

Let’s prepare a flow chart.

Situation: Economy has inflationary trend. Prices of goods and services increasing every day.

Solution: RBI raised reserve ratio (CRR, SLR)

Result: SBI is left with less money to lend.

Consequences:

- SBI raises its loan interest rate

- Businessmen borrow less money from SBI

- Businessmen donot start new business. Donot expand existing business

- Result=Less jobs. Even existing employees discharged. If anyone remains in the job, he doesn’t get pay raise. He starts cutting down unnecessary expenditure (e.g. buying two newspapers, getting his shirts ironed, drinking tea @4PM in office and so on. Thus even paper-wall, dhobi, chai-walla- everyone’s income reduced.)

- Result= Less income (Because of above reasons)

- Result= Less demand of goods and services (because less income).

- Ultimately shopkeeper will bring down the prices to attract people into buying more things.

Thus inflation is reduced.

You may doubt- what about supply side bottlenecks, what about cost push and demand pull inflation : I’m not going into all that details at the moment, else this article will become longer than five kilometers.

Let’s just prepare a summary table:

| Policy | dear money | cheap money |

|---|---|---|

| Tool | To fight inflation | To fight deflation |

| Reserve Ratio (CRR, SLR) | Increase them. | Decrease them. |

Moving to the next (Quantitative) tool. Under monetary policy

#2: Open Market Operation (OMO)

- Open Market Operation= when RBI starts buying/selling government securities to control money supply.

- Government securities= piece of paper. It says something like this “give me Rs.100, I’ll give you 8% interest rate for next ten years and after that I’ll repay the principle of Rs.100.” This is how government borrows from others.

- Situation: Economy has inflationary trend. Prices of goods and services increasing every day.

- Solution: RBI starts selling government securities in open market.

- Result: SBI buys them and thus SBI’s lending money is reduced. Wait. How?

Imagine Rajan is selling “sabzi” (vegetables). If SBI’s chairman Arundhati Madam goes to buy vegetables. Obviously madam’s money will decrease when she buys vegetables.

Then same as usual:

- SBI left with less money to lend.

- SBI raises its loan interest rate (to keep profit margin same)

- Businessmen borrow less money from SBI.

- Businessmen donot start new business. Donot expand existing business

- Less jobs

- Less income

- Less demand

- Ultimately shopkeeper will bring down the prices to attract people into buying more things.

Thus inflation is reduced.

During deflation, RBI will do the reverse. (i.e. RBI buys “Sabzi” from SBI). How will it stop deflation? Think in your head.

Let’s update our table

| Policy | dear money | cheap money |

|---|---|---|

| Tool | To fight inflation | To fight deflation |

| Reserve Ratio (CRR, SLR) | Increase them. | Decrease them. |

| Open Market Operation (OMO) | RBI sell securities | RBI buy securities |

Mock Question

In 2013, UPSC walla asked a very chillar question from this topic.

In context of Indian Economy, ‘Open Market Operation’ refers to

- Borrowing by scheduled banks from RBI

- Lending by commercial banks to industries and trade

- Purchase and sale of government securities by the RBI

- None of Above

Whenever you face a GS/GK type MCQ, You’ve three choices

| Skip | If you don’t know the answer, Just leave it instead of risking negative mark. |

| Attempt | Correct answer is Opt C. |

| Mark n Review. | It means you’ve unsure of the answer. 50:50. So you mark the question number (say 45), at the back of your question paper. At the end of exam, if you’re left with 10-15 free minutes. You look at the question again, and try to solve it. |

So, should you put above question in “mark n review”?

- No.

- Because it’s a definition based question. If you don’t know the definition of “OMO” you might tick a wrong answer and fail. Most of the sincere players fail in prelims because of this reason. They push their luck in negative marking to overcome an ‘imaginary’ cutoff and thus dig up their own grave. (especially during last 10-15 minutes of the exam.)

- Moral of the story: never put “fact/definition” type MCQs in Mark-n-Review.

Let’s solve a bit more complicated MCQ from 2012’s CSAT paper.

Q.Which of the following measures would result in an increase in the money supply in economy?

- Purchase of government securities from public by central bank

- Deposit of currency in commercial banks by the public

- Borrowing by government from the central bank.

- Sale of government securities to the public by central bank.

Answer choice

- Only 1

- 2 and 4

- 1 and 3

- 2, 3 and 4

Whenever you face such multiple statement type MCQs, always use “elimination method”. First find a statement that is definitely right or definitely wrong and eliminate choices accordingly.

- Focus on first statement “Purchase of government securities from public by central bank”: will it increase money supply in the system?

- Imagine Rajan puts an ad in newspaper: bring your Sabzi (vegetables), I’ll buy it. Junta gives him their own veggies, Rajan gives them money. (a classic buy and sell).

- Ultimate result: money supply increased in the system- because junta got the money. Meaning #1 definitely correct.

- If you think it on technical terms. Central bank purchases government securities=OMO (Open market operation), where money shifts hands from RBI to people.

- Hence money supply increased. (In reality, money doesn’t go to ‘aam admi’ directly, but those bankers and non-banking institutions who participate in OMO). Anyways, #1 is right, Eliminate choices that do not have #1

- Only 1

- 2 and 4

- 1 and 3

- 2, 3 and 4

Now the final answer depends on whether statement #3 is right or wrong?

- Statement #3 says “Borrowing by government from the central bank.” (So, will it increase money supply?)

- How does Government borrow from Central bank? Does Mohan just callup Rajan and demand 1 lakh crores? No. Mohan will have to give Rajan that much government securities (vegetables) and Rajan will give him cash.

- Is money supply increased? Yes Mohan sold veggies to Rajan and got Money. Whenever Rajan buys veggies and pays – the money supply is increased. (this is similar to Open Market operation)

- Besides, Mohan can then use money to pay salaries of government staff, pay for rail-road-bridges and other infrastructure projects, pay for MNREGA and so on. Therefore Answer C: 1 and 3 correct.

Counter- argument?

- What if Rajan subsequently sells those (Mohan’s) securities to bankers. Then banker’s money reduced. Hence #3 is wrong. Therefore final answer A only 1.

So, what’s the final answer: is it A or is it C?

Ultimate judge= UPSC’s official answer key uploaded on their site.

In 2012’s Question paper Test series “A”, this is Q77: and its official answer is “C”. Therefore, both 1 and 3 are correct.

Anyways, what to do in the exam?

| Skip | If you don’t know the concept better skip. |

| Attempt | This question is attemptable if you don’t drag the logic too much in statement #3. |

| Mark n Review. | Yes, it can be put under “mark and review” because this is not an absolute fact/ absolute definition type MCQ. If you apply some concepts, you can eliminate wrong choices. But still if doubt persists in the mind (e.g whether Statement 3 is right or not) then it’s always safe to skip and avoid negative marking. |

By the way, What about Statement #2: Deposit of currency in commercial banks by the public. (Will it increase money supply or not?)

- Viewpoint 1: yes. Because bank can used it to expand loanable credit. (as explained in Money creation topic in Class 12 NCERT Macroeconomics page 39 onwards).

- Viewpoint 2: no. (Because Bank will have to put some money aside as CRR- so that much money is less in the system.)

Either way it doesn’t change the answer. Because We know that statement 1 is definitely correct. And there is no option where (1,2) are given simultaneously.

Anyways, Moving on…So far, RBI has two tools under monetary policy:

- reserve ratios (SLR, CRR)

- Open market operation.

Third and the most important “quantitative” tool is

#3: Policy Rate

“Policy rate”= in case of India its Repo rate. Before moving further, let’s refresh our concepts of Bank rate, LAF, MSF, Repo and Reverse repo.

Bank Rate

- When banks borrow long term funds from RBI. They’ve to pay this much interest rate to RBI. [Note: different books give different explanation of Bank Rate. I’ve used NDTV’s definition]

- At present, Bank rate= 9%

- Collateral: nothing. (Bank can borrow money without pledging government securities to RBI)

- Bank rate is not the main tool to control money supply these days.

- Nowadays, RBI uses LAF Repo rate as the main tool, to control money supply.

Ok then What’s the use of Bank rate?

- Penal rates are linked with Bank rate. For example, If a bank doesn’t maintain CRR, SLR as per the prescribed limit.

- Then RBI can impose penalty interest on such notorious bank.

- At present, Penalty rate = Bank rate + 3% (or 5% in some cases)

- Meaning if Bank rate = 9% then penalty rate=9+3=12%

Anyways, what if RBI wants to fight inflation using bank rate as a “tool”?

Obviously they should increase bank rate. That way it becomes harder (more expensive) for banks to borrow from RBI.=> SBI increases its loan rates (to keep the profit margin same). Result?

- Less people get home loan, bike loan, business loans.

- Less business expansion

- Less jobs

- Less incomes

- Less demand

- Ultimately shopkeeper will bring down the prices to attract people into buying more things.

Thus inflation is reduced.

Let’s update our (stupid) table

| Policy | dear money | cheap money |

|---|---|---|

| Tool | To fight inflation | To fight deflation |

| Reserve Ratio (CRR, SLR) | Increase them. | Decrease them. |

| Open Market Operation (OMO) | RBI sell securities | RBI buy securities |

| Bank rate | Increase | decrease |

Liquidity Adjustment facility (LAF)

- Liquidity Adjustment facility

- RBI started this in 2000. You can imagine it as a “Adda/gambling den/gang-hideout” where RBI’s clients gather, consumer desi liquor, play cards, watch item songs and borrow money from RBI (or lend Money to RBI).

- By the way, who are the clients of RBI?= Central and state governments, Banks and non-banking financial institutions (NBFI). NBFI further includes:

- AIFI (all India finance institutions) NABARD, SIDBI, EXIM Bank and National Housing Bank.

- Primary dealers (Morgan Stanley , Goldman Sachs, JP Morgan Chase, Standard Chartered Bank, HSBC etc.)

- Non-Banking financial companies.

- Anyways, Under this LAF “adda”, RBI has two tools:

| Repo | If client borrows money from RBI (for short term) then client has to pay this much interest rate to RBI. At present Repo is 8%. (article written on 29th Jan 2014) |

| Reverse Repo | If client lends money to RBI (for short term) then RBI has to pay this much interest rate to client. RBI doesn’t like headache. So they made a simple formula: Reverse repo rate= Repo MINUS 1%=8-1=7%. |

Collateral:

- Problem with running a “adda/gambling-den” = sometimes client drinks too much desi liquor and passes out on floor. Sometimes he even dies because of ‘hooch’. Sometimes police raids the den, and clients run away with cash and register.

- If such things happen, Rajan will be at loss. So, he demands “government securities” as collataral. So even if client doesn’t repay money on time, Rajan can sell those securities (in open market operations) and recover money.

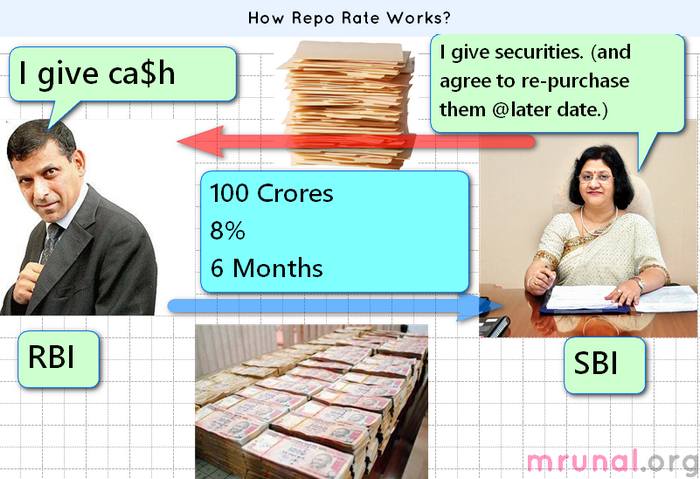

LAF Repo Rate

Let’s get a bit technically correct now. Observe following image

Scenario

- SBI chairman Arundhati ma’m wants to borrow Rs.100 crore (for short term).

- She gives her stash of government securities to Rajan.

- Rajan gives her Rs.100 crore.

- Madam Also signs an agreement

- “I, Arundhati Bhattacharya, agree to buy same securities from Rajan, at 108 crores after 14 days.”

- Notice that she has agreed to “re-purchase” same securities from Rajan. Therefore its called “Repo.”

- And how much interest rate did she pay on this “loan”? [108-100]/100=8%. That’s our repo rate.

- Important:

- Recall that SBI also has to keep part of her money in RBI approved securities (under SLR).

- So Madam cannot USE those government securities to borrow under Repo Rate from Rajan.

That leads to a new topic

Marginal Standing facility (MSF)

| LAF (Repo) | MSF |

|---|---|

| Rajan says “don’t come here unless you want to borrow minimum Rs.5 crores.” | Minimum Rs. 1 crore. |

All clients are welcome i.e.

|

|

| You (bankers) cannot pledge securities from SLR quota to borrow from this window. | Can use securities from SLR quota. |

| No limit. You may borrow as much as you want. (as long as you have government securities to pledge to me.) | Maximum 0.75% of NTDL. To put this in crude words, if SBI received 100 crores from aam-admi under savings account, current account, fixed deposit etc. then SBI can borrow only upto Rs.75 lakhs from RBI. |

| Rajan decides Repo rate (8% right now) | MSF = Repo Rate +1% = 8+1=9%. (earlier this margin of 1% used to be higher. But nowadays just 1%!) |

for those who still have doubt about Repo vs MSF:

for repo borrowing, bank will need to pledge securities to Rajan. But bank cannot use SLR-reserved securities for this.

so, imagine if a bank is in dire need of cash, but doesn’t have spare government securities- then they can borrow using MSF by pledging those SLR securities. (and under MSF window, Rajan will demand 1% higher than Repo as one type of ‘punishment’ for pledging SLR securities.)

Reverse repo Rate

- Although self-explanatory. But let’s check

- Repo = clients borrow from Rajan and pay this much interest rate. (short term loan)

- Reverse repo= when Rajan himself borrows from clients, then he has to pay this much interest rate to clients.

- Collateral = yes. What if police raids this gambling-den, and Rajan runs away to Nepal? Clients can sell Rajan’s Government securities and recover their money.

- Reverse repo = Repo MINUS 1% = 8-1% =7%.

- Note: in official parlance, they call percentages in “basis points” so 1%=100 basis points. So in that ‘official language’, Reverse repo = Repo MINUS 100 basis points.

Enough cheap jokes. What have we learned so far?

- That Rajan controls money supply using monetary policy.

- Under Monetary policy, Rajan has various “weapons” (or tools)

- Reserve ratios (SLR, CRR)

- OMO: Open market operation

- Rates: Bank rate, LAF (Repo, Reverse repo), MSF.

We already know how to apply SLR, CRR and OMO to fight inflation (and deflation.) let me paste the table again.

| Policy | dear money | cheap money |

|---|---|---|

| Tool | To fight inflation | To fight deflation |

| Reserve Ratio (CRR, SLR) | Increase them. | Decrease them. |

| Open Market Operation (OMO) | RBI sell securities | RBI buy securities |

| Bank Rate | increase it | decrease it |

| Repo rate | increase it | decrease it |

| Reverse Repo | it’s value is linked with Repo, hence cannot be increased/decreased independently. | |

| Marginal Standing Facility | it’s value is linked with Repo, hence cannot be increased/decreased independently. Besides MSF= temporary firefighting, cash mismanagement. | |

- We learned that Rajan doesn’t use Bank rate much, to control money supply.

- We learned that Rajan doesn’t decide Reverse repo and MSF. (they’re automatically -1% and +1% of Repo rate).

- Thus the only thing Rajan has to decide under monetary policy= Repo rate. Therefore, Repo rate is called the “policy rate”

Let’s revisit out flow chart:

- Situation: Economy has inflationary trend. Prices of goods and services increasing every day.

- Solution: Rajan increases “Repo rate”. (say from 7.75% to 8%).

- Result: it becomes expensive for SBI to borrow from Rajan. They’ll increase their own rates as well.

- Wait. How?

Just like how things roll in Onion biz.

If prices of Onion rise in Maharashtra’s wholesale yard (in Lasangaon), then immediately, retail veggie @Ahmedabad will also raise their onion prices to keep the profit margin same.

What’ll be the consequences (if repo rate is hiked / increased)?

Consequences:

- SBI raises its loan interest rate (to keep profit margin same)

- Businessmen borrow less money from SBI.

- Businessmen donot start new business. Donot expand existing business.

- Less jobs

- Less income

- Less demand

- Ultimately shopkeeper will bring down the prices to attract people into buying more things.

Thus inflation is reduced.

| Policy | dear money | cheap money |

|---|---|---|

| Tool | To fight inflation | To fight deflation |

| Reserve Ratio (CRR, SLR) | Increase them. | Decrease them. |

| Open Market Operation (OMO) | RBI sell securities | RBI buy securities |

| Policy Rate (Repo Rate) | Increase it | Decrease it |

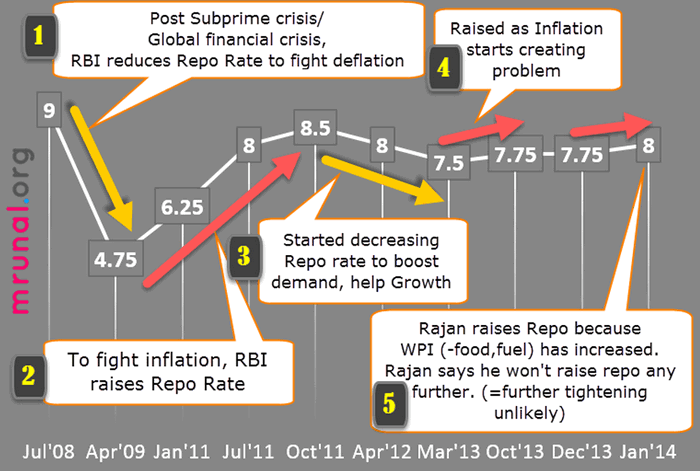

Repo Rate in recent years:

Let’s observe with a graph: how RBI fought inflation/deflation in recent times using Repo rate as the “main-weapon” of monetary policy.

From above above graph, you can see RBI has frequently changed its repo rate to combat both inflationary and deflationary trend. But You’d agree that inflation has not been contained. No matter what number juggling or statistical interpretations are given- the hardship of common man has not stopped- be it milk, petrol, onion, LPG anything.

- Agreed that prices of onion, sugar, pulses and food are subject to vagaries of monsoon and black marketeering. Rajan cannot do anything about it.

- Agreed that crude oil prices are subject to rupee-Dollar exchange rate, external factors and government’s de-regulation of their prices. Rajan doesn’t have much control over this.

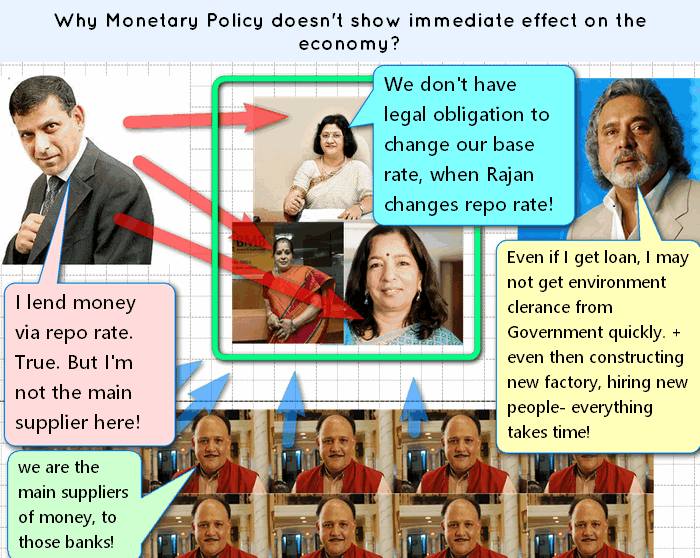

But still even in the non-food, non-fuel type commodities- RBI’s monetary policies have failed to curb inflation. WHY? Observe the following image.

Suppose Vijay Mallay got 100 crore loan from State Bank of India. If you trace the ‘source’ of that money, it’ll turnout 60-70 crores came from bank’s savings account, fixed deposit etc. Rajan lends money in repo rate –yes, but that doesn’t mean banks depend only on Rajan to arrange the cash for its clients.

Suppose Rajan reduces repo rate from 8% to 5%. Banks are not legally required to reduce their loan interest rates.

- The current system is following:

- Banks are free to decide their base rate. E.g. SBI’s base rate is 10%.

- It means SBI won’t loan money to anyone at an interest rate lower than 10% (except those farmers under Interest subvention scheme.)

- SBI will link all of its loan products with Base rate. For example

| SBI Base rate =10% | Calculation | Result |

| Car loan | 0.75% above Base rate | 10.75% |

| Two wheeler loan | 8.25% above base rate | 18.25% |

| Education loan (upto 4 lakh) | 3.5% above base rate | 13.5% |

| Home loan for women (upto 75 lakh) | 0.10% above base rate | 10.10% |

Meaning if SBI changes her Base rate then all of above loan interest rates will change automatically.

If Rajan changes his repo rate, will SBI change her base rate?

Not always.

- Because those common men are the main suppliers of money to SBI.

- RBI is not the main supplier of money to SBI.

- SBI will only change its base rate, when she feels necessary for its own profit / loss compared to its competitors.

Does it mean Repo rate system is bogus and ineffective?

Not always.

- In developing countries like India, most people park their money in only four things: savings account, fixed deposit (FD), provident fund and LIC. We’ve mutual funds, we’ve NPS, we’ve ULIPs, we’ve Rajiv Gandhi equity savings scheme –

- but most people (particularly the older generation) feels insecure in into such new things. Therefore lot of money flows into Savings accounts and fixed deposits= SBI’s main source of money.

- But, In advanced economies, like USA, people don’t invest large portion their income in savings account or FD. They’ve variety of investment options. So, for those American banks, their own Central bank (US Feds) is a significant money supplier.

- Hence US Feds’ monetary policy shows faster impact on their American Banks, THAN Rajan’s monetary policy on Desi banks.

Monetary Policy: limitations

In developing countries, Monetary fails to bring quick results because

- People don’t have many investment alternatives. Commercial banks have large deposits. Rajan is not the main or even prominent money supplier for these banks. Whatever Rajan does, its effect will be felt only after 6-8 months but by that time, new factors would cause another rise in inflation and Rajan will have to start from scratch again.

- Non-Monetized economy: in rural areas, many transactions are still of barter nature. (E.g. kiranawalla cum middleman supplies seeds, pesticides, fertilizers- in exchange of share in farmer’s produce.)

- Lack of financial inclusion. Since most people are not in the banking net. They rely on Shroffs and moneylenders. Many of them circulate the black money of cops and politicians, and charge 36% interest rate on loans. Rajan has no control over them.

- Monsoon uncertainty, cyclone, flood, draughts and their effect on food production. Food inflation =>newspaper walla, washerman, barber, car mechanic everyone will raise their service fees to accommodate their raised cost of living. Rajan has no control over them.

- Crude oil and gold import + negative effect when rupee weakens. Rajan can try to bring 1$=Rs.65 to $1=63 Rs. But he has not enough forex reserves to bring $1=Rs.50.

- Fiscal deficit, illogical schemes. e.g MNREGA worker digs a temporary road. After first rain, t he road is wiped out= physical infrastructure added to economy… no. Wages raised…..yes. = this mismatch leads to more inflation.

- Subsidy leakage, Black money, underground economy.

- And most importantly, because Rajan uses Multi-indicator approach, he focuses on WPI (minus food and fuel). That’s why Urjit Patel recommends him to target CPI. More on that in next article.

So far, we learned that RBI has two sets of tools/instruments under monetary policy:

| Quantitative tool | Qualitative tools |

|---|---|

|

We’ll see them in a moment |

Qualitative Tools

#1: Margin Requirements/ LTV

- Mallya wants to borrow from SBI. He pledges his company’s shares worth Rs.100 crores as collateral.

- For such loans, Rajan can prescribe margin, say 65%.

- In that case even if Mallya pledges 100 crores worth shares, SBI can give him 100-65=only 35 Crore rupees as loan.

- Using this tool, Rajan can control money supply. e.g. during inflation, he should increase margin requirement, so Mallya can borrow less=> less job=>less income=>less demand=>prices reduced.

- If Rajan changes repo rate, it is not compulsory for SBI to change her loan interest rates. (we saw how Alok Nath keeps giving money to SBI, so they are not entirely dependent on Rajan.)

- But if Rajan changes margin requirements, then SBI and all other banks must obey it. In other words, this tool has direct impact on money supply.

#2: Consumer credit regulation

- Suppose Nano car sells @1 lakh and Rajan has made rule that downpayment cannot be less than 30%.

- It means customer must bring Rs.30,000 from his pocket and bank can only give him maximum 70000 as loan.

How can Rajan fight inflation with this tool?

- Increase downpayment from 30%=>50% (meaning bank can give less loan. Customer himself has to arrange lot of money from his own pocket)

- Rajan can make rule “banks cannot accept EMI less than 5000 on car loan.” Observe:

Case #1: 100 EMIs worth 1000 each = 1,00,000. (ignore interest rates)

Case #2: 20 EMIs worth 5000 each=1,00,000. (ignore interest rates)

In case #2: some of the lower-middleclass families may postpone their decision to purchase nano car (Because they can’t afford higher EMIs.)

- Result= less demand=>prices reduced. (indirectly- because car mechanics get less work, number-plate painters get less orders etc. so they reduce fees to attract new clients and retain existing clients.)

- Thus, Rajan can control money supply by changing downpayment and installment (EMI) rules.

#3: Selective credit control

- Under this, Rajan can specifically instruct bankers not to give loans to traders of certain commodities e.g. sugar, gur, edible oil etc.

- even if the said trader is ready to mortgage his shares/bonds/factory/machine/vehicle anything.

- this prevents speculations/ hoarding of commodities using money borrowed from banks.

#4: Moral Suasion

Here Rajan tries to persuade the bankers to do xyz thing. Example

- Please reduce giving automobile loans- instead park your money in government securities. (above the SLR requirements.)

- I’ve reduced my repo rate, now you also reduce your base rate.

Rajan will try to influence those bankers via- direct meetings, conference, giving media statements, giving speeches @public seminars, university convocations etc. (even where bankers are not present.) He’ll do so, to build a public opinion, media opinion and influence those bankers by making them feel ‘guilty’.

| Rationing of credit |

|

|---|---|

| Direct action | Means RBI gives punishment to erring banks. Punishment can involve: penal interest, refuses to lend them money from LAF etc. and in worst case even cancels their banking license. |

Let’s recap

Let’s solve an Official MCQ from UPSC 2012 Question paper

Q. RBI Acts as banker’s bank. This would imply which of the following?

- Other banks retain their deposits with RBI

- RBI lends funds to commercial banks in the times of need.

- RBI advises commercial banks on monetary matters.

Correct Statement

- Only 2 and 3

- Only 1 and 2

- Only 1 and 3

- 1, 2 and 3

Approach:

Whenever you face such 3 statement MCQ or 4 statement MCQ, Always use “elimination” method. First you find out a statement that is definitely right or definitely wrong. In above case, we can see #2 is definitely right. RBI lends funds to banks in the times of need (Repo, MSF)

So let’s eliminate choices that don’t involve statement #2

- Only 2 and 3

- Only 1 and 2

- Only 1 and 3

- 1, 2 and 3

- This did not help much. We still have three choices left. Observe statement #1: Other banks retain their deposits with RBI. That is correct with respect to cash reserve ratio. CRR is one type of deposit that banks make to RBI. (RBI doesn’t pay interest on it- that’s a different story).

- Meaning #1 is also correct eliminate choices that donot have #1

- Only 2 and 3

- Only 1 and 2

- Only 1 and 3

- 1, 2 and 3

Only two choices left and the ultimate solution = is statement #3 is correct or not?

| Viewpoint #1 | Viewpoint #2 |

| The statement says “RBI advises commercial banks on monetary matters.”The word “advises” makes this statement incorrect. Because RBI doesn’t “Advice” they just order the banks- be it SLR, CRR, PSL. RBI doesn’t advice, RBI gives orders and direction. Therefore statement #3 is wrong. | RBI does advice those banks. We saw it under “Moral Suasion.” Therefore, Statement #3 is right. |

| Even if we accept that RBI “advices”, still the questions asks what is implied by “RBI as Banker’s bank.” So, RBI advices “moral suasion” that is a monetary policy tool. RBI’s not doing it as a “Banker” to those banks. Therefore, Statement #3 is definitely wrong. | Money Banking and finance, E Narayan Nadar (PHI publication). He has specifically listed this “Advice” function under Banker’s bank topic. |

| Answer (B) | Answer (D) |

- So, is it B or is it D? Final judge is UPSC.

- They had uploaded CSAt-2012 official answer key on their site.

- This question is Test Series A, Question #75 and its official answer is “D” = meaning all three statements are correct.

If you face such MCQ in exam, what should be your approach?

| Skip | Upto you. But if you start skipping all such question (OMO, Money supply, Banker’s bank), because you’re completely unaware of those topics=that is not pardonable.it shows you’re underprepared for this exam. You should either change your study method or change the game- try for some easier exam. |

|---|---|

| Attempt | This question is attemptable, if you don’t ‘nitpick’ over the word “advises” in third statement. |

| Mark n Review | If you’ve thoroughly prepared the RBI’s monetary tools (both qualitative and quantitative), you can solve it by applying concepts/principles- particularly the moral suasion thing. But if you’re still doubtful over whether #3 is right or wrong, then better skip. If you skip because you’re ‘doubtful’ = that is pardonable. But if you skip because you’re completely unaware of this topic= non-bailable offense. |

Appendix

These are the topics I wanted to discuss in the article, but they would break the flow of other topics. Hence writing them @bottom:

#1: Why High SLR and High CRR are bad?

From the discussion so far, you might think why Rajan only focuses on Repo rate to control money supply. Why not simply raise SLR and CRR requirements.

Let’s check the de-merits of high SLR and CRR:

Prior to LPG reforms in 90s, RBI used to keep SLR and CRR very high. Let’s take an example

A Bank can two types of deposits

| Deposit type | examples |

| Time Deposit | Fixed deposit (FD) recurring deposit. |

| Demand Deposit | Savings account, current account |

- Using this money, bank has to count its Net Demand and Time liabilities (NDTL), every fortnight. Suppose its 100 crores.

- Both CRR and SLR are counted on this figure. In the old times, these reserve ratios used to be as high as 15% and 40% respectively. Observe the effect:

| Net Demand and Time Liabilities (NDTL) | +100 cr. |

| Reserve ratios | |

|---|---|

| CRR (15%) | (-) 15 [no profit] |

| SLR (40%) | (-) 40 [some profit] |

| Money left with bank | =45 cr. |

From 100 crores, barely 45 crores left with the bank. But adding insult to the injury- even here RBI mandates Priority sector lending (PSL). Meaning, at least 40% of the loans has to be given to farmers, small businessmen, students etc. groups.

Let’s update the table:

| Net Demand and Time Liabilities (NDTL) | +100 cr. |

| Reserve ratios | |

|---|---|

| CRR (15%) | (-) 15 [no profit] |

| SLR (40%) | (-) 40 [some profit] |

| Money left with bank | =45 |

| PSL (40%) | =45 x 0.4 =18 crore. |

| Money left for big borrowers (i.e. big businessmen, upper middleclass) | =45-18=27 crores. |

- By the way, PSL is counted on annual basis while SLR, CRR counted on fortnight basis so above table is technically incorrect but I’ve plugged in those numbers only for the sake of explanation.

- before the 90s- Government would even interfere and order public sector banks to give PSL-loans @cheap interest rates. The local politicians would coerce the branch manager to give PSL-loans to ineligible people. They default on loans, Branch manager cannot recover money (because defaulter will goto civil court then taarikh pe taarikh.) So, bank would have to forget about most of those 18 crores given in PSL loans.

- Anyways you can see people deposited 100 crores in the bank yet bank is left with barely 27 crores (over which, bank has “Freedom” to decide whom they should give the loan.)

What are the consequences for businessmen?

- High cost of credit (because bank will try to make maximum profit from those 27 crores- so bank will charge very high interest rate on the business loans- to pay off for the staff salaries, branch office rents and everything.)

- Businessman cannot expand his business.

- Less exports.

- Less tax income for the government.

So in a way- that was also one of the factors leading to Balance of Payment crisis (and subsequently LPG reforms.) You can read more about that in NCERT Class 11- chapter 2 and 3.

#2: Narsimhan (I) Committee 1991

Plagued by problems and losses in nationalized banks, Government of India formed this Committee. Recommendations were:

- Deregulate interest rates. Let the banks decide their loan interest rates. Accepted. Gradually, we moved to the Base Rate system.

- PSL loans should be given at normal interest rates. Accepted (but with exception=> interest subvention- that we saw under Nachiket articles.)

- NPA/Loan default matter should be handled by separate body and not civil courts. Result: Debt recovery tribunal created in 1993. Ultimately SARFAESI Act in 2002.

- Reduce CRR, SLR. Accepted. Today we’ve them @4% and 23% respectively.

- Allow Private banks and foreign banks. RBI invited applications in 1993. ICICI, Axis, HDFC and many others got license.

- Liberate Branch expansion policy. Done (Except that 25% rural branching mandate we saw under Nachiket articles).

- Prepare NBFC regulatory framework. Accepted.

- Government should reduce shareholding (and thereby its official influence) in the public sector banks. Government agreed. Today government’s shareholding in SBI =~60%.

#3: Narsimhan (II) Committee 1998

Suggested more reforms.

- allow VRS in the banks so they can get rid of excessive staff.

- Suggested additional Legal reforms for loan recovery. =>SARFAESI 2002.

- Computerization, electronic fund transfer, legal framework => Payment and Settlement Act=>Retail (ECS, NEFT, credit Card) + Wholesale (RTGS)

- Permit new private /foreign banks. RBI invited license in 2001= Yes Bank and Kotak Mahindra got licenses. 2013: RBI again invited applications for bank licenses.

[Note: list of recommendations not exhaustive, I’ve only highlighted important topics that show ‘evolution’ of banking sector in recent times.]

Mock Questions

- With open market operations, RBI can

- increase liquidity in the economy, but cannot decrease it

- decrease liquidity in the economy, but cannot increase it

- Can increase or decrease liquidity in the economy to control money supply.

- None of above.

- By which of the following methods, government can reduce money supply in the economy?

- taxation

- sale of securities to public

- both A and B

- neither A nor B

- During the period of deflation

- RBI should use dear money policy to combat it

- Government should reduce its tax rates.

- both A and B

- Neither A nor B.

- IF prices are lowered without causing unemployment, we call it:

- stagflation

- reflation

- disflaction

- Disinflation.

- Which of the following contains correct set of quantitative instruments of monetary policy?

- reserve ratio, bank rate, margin requirements

- open market operations, margin requirements, regulation of consumer credit

- cash reserve ratio, bank rate, open market operation

- None of above

- Which of the following contains correct set of qualitative instruments of monetary policy?

- reserve ratio, bank rate, margin requirements

- credit rationing, margin requirements, regulation of consumer credit

- cash reserve ratio, bank rate, open market operation

- None of above

Q7. To counter the effect of deflation, which of the following steps should RBI initiate?

- decrease reserve ratios

- buy government securities through open market operation

- increase policy rate

Answer choices

- only 1 and 2

- only 2 and 3

- only 1 and 3

- 1, 2 and 3

Q8. To counter inflation, which of the following steps should RBI initiate?

- Increase reserve ratios

- sell government securities through open market operation

- Increase policy rate

Answer choices

- only 1 and 2

- only 2 and 3

- only 1 and 3

- 1, 2 and 3

Q9. Which of the following may cause deflation in the economy?

- RBI raises policy rate

- RBI raises cash reserve ratio

- RBI sells securities

Choices:

- only 1 and 2

- only 2 and 3

- only 1 and 3

- all 1,2 and 3

Q10. Money supply in the economy, is affected by

- Cheap money policy and dear money policy.

- Open market operation and Moral Suasion.

- Consumer credit regulation and loan to value ratio.

Choices:

- only 1 and 2

- only 2 and 3

- only 1 and 3

- all 1, 2 and 3

Q11. An increase in SLR

- will restrict the expansion of bank’s credit

- will increase bank’s investment in safe securities

- will ensure solvency of the banks

choices:

- only 1 and 2

- only 2 and 3

- only 1 and 3

- all 1,2 and 3

Mains/interview type questions- after we check Urjit Patel’s recommendations on strengthening monetary policy.

Hints

- can increase by buying, can decrease by selling

- both [or only B, depending on how UPSC examiner interprets the effect of taxation on money supply. In one of the reputed book on Banking and finance, author Narayan Nadar claimed taxation can affect money supply.]

- dear money policy during deflation =adds insult to the injury of businessman. If government reduces tax- then its revenue collection will drastically reduce. So both incorrect. [OR debatable- depending on how UPSC examiner interprets the effect of taxation during deflation.]

- directly given in the article.

- see the last table in the article

- see the last table in the article

- observe the table before the topic “repo rate in recent years”

- same as above

- same as above

- All correct. (Unless you nitpick and drag the logic too much.)

- same as above.

Visit Mrunal.org/Economy For more on Money, Banking, Finance, Taxation and Economy.

![[Win23] Economy Pill4ABC: Sectors: Agri, Mfg, Services, EoD, IPR related annual current updates for UPSC by Mrunal Patel](https://mrunal.org/wp-content/uploads/2023/04/win234b-500x383.jpeg)

When RBI varies Reserve Ratios to fight inflation or deflation , banks change their Interest Rates to keep their profit margin stagnant.

It’s the seller who really have to compromise with the profit(he have to bring down the S.P to increase the sale in time of inflation).

Is it a good thing or is there any other way of interpreting this?

Mrunal Sir I understand that keeping money with RBI under Reverse Repo rate doesn’t make sense as the bank can surely find better interest rate takers in the market. But let us suppose the policy rate is sufficiently high and the bank considers it safe to put some money under Reverse Repo with RBI, can it put any amount that it wants, or can it “invest” in RBI, even for a short time? Because the facility decision I guess lies with RBI whether to sign a Reverse Repurchase agreement or not. Please clarify

Superb explanation. Mind Blowing! Thank you so much Mrunal.org.

thank you for this simple explanation sir….

Its really awesome…thank you so much sir

Unbelievable explanation. If one want to understand economics it will help him the most.

Thanks a lot sir with the core of my heart

Awesome…

This guy is really good. Thanks a lot Sir :)

Sir, u are excellent in making simple examples and in clearing the fundamentals of the concepts. I appreciate your each video lecture also.

Thanks Sir.

just captivating,,, this is the way every explanation and example needs to be

your teaching technique is too good sir.

I get to understand the economy for the first time since I started my preparation….