- NPA / TBS problem: three stages of

- What is SARFAESI Act 2002?

- Why insolvency and bankruptcy code 2016?

- Banking Regulation (Amendment) Ordinance, May 2017

- PNB Scam: LoU & SWIFT

- Public credit registry (PCR)

- Legal Entity Identifier (LEI)

- FRDI bill

NPA / TBS problem: three stages of

- Till mid-2000s: Corporates were taking large amount of loans. []

- 2007-08: after the global financial crisis, UPA government’s policy paralysis & judicial activism there were bottlenecks in economic activities. Companies had difficulty in repaying the loans.

- By 2013: nearly 1/3rd of the bank loans were owned by IC1 companies i.e. companies not generating enough revenue even to repay the loan interest.

Thus, companies with weak balance sheets led to public sector banks with weak balance sheets. It is called “Twin balance sheet syndrome” (TBS)

NPA related definitions

| Term | If principal or interest is not paid for a period of: |

|---|---|

| SMA-0 (special mention account) | 1-30 days |

| SMA-1 | 31-60 days |

| SMA-2 | 61-90 days |

| NPA (non-performing asset) |

|

| Substandard asset | When a loan account remains in the NPA classification for 12 months or more |

| Doubtful asset | When an NPA account remains in the substandard classification for 12 months or more |

| Loss Asset | When Bank, its auditor or RBI says that given doubtful asset has little / no salvageable value. |

| Loan write-off |

|

| Restructured loan | When principal / interest rate / tenure of the loan is modified. |

| Stressed asset | NPA + loans written off + restructured loans = stressed assets |

| OTS with haircut | If bank allows the client to pay 60% of dues and forgoes 40% as loss, then we say bank has offered “onetime settlement with 40% haircut” |

| Ever-greening | Taking a new loan to pay off the old loan. |

RBI “3R” Framework for Revitalizing Stressed Assets

| Rectification |

|

| Restructuring (2014-16) | Loan interest (%), tenure or ownership could be changed.

RBI has stopped these schemes from 31 March 2018. Now banks can restructure loans only under the provisions of insolvency and bankruptcy code 2016. |

| Recovery | Bank liquidates the assets of the company under:

|

(UPSC-Prelim-2017) ‘Scheme for Sustainable Structuring of Stressed Assets (S4A)’ is related to:

- procedure for ecological costs of developmental schemes

- scheme of RBI for reworking the financial structure of big corporates with genuine difficulties.

- disinvestment plan for Central Public Sector Undertakings.

- Provision in ‘The Insolvency and Bankruptcy Code’

What is SARFAESI Act 2002?

- 1991: Narsimhan Committee on banking sector reforms observed clients obtain stay orders from ordinary courts, therefore, banks have difficulty recovering the NPA

- 1993: debt recovery tribunals (DRT) were set up, so ordinary courts can’t interfere in the loan recovery process.

- 1998– Narsimhan-II Committee observed that DRT need to be strengthened with a law.

- 2002: Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act was enacted.

- Under this act, banks and housing finance companies (NBFCs) can attach the mortgaged assets when loan is not repaid. They can auction / sale / change board of directors in such assets / companies. They can also sell such assets to asset reconstruction companies (ARC). These provisions are not applicable on the farm loans though.

- If client wants to obtain a stay order, he cannot go to ordinary courts. He will have to approach for debt recovery tribunal (DRT), with application fees ranging from 12,000 to 1.5 lakh depending on the loan amount. DRTs are understaffed, over 1 lakh cases are pending (2016), and Rs.1.5 lakh is a small fee for large corporates. So, case will go on for years and the debtor will remain in possession of the asset.

- If DRT doesn’t give stay order, then client can appeal to debt recovery appellate tribunal (DRAT), but DRAT will require him to deposit minimum 50% of the loan dues.

Why insolvency and bankruptcy code 2016?

- Because, SARFAESI-DRT understaffed so recovery is time-consuming, Debtor remains in possession, which leads to erosion of asset-value (machinery, vehicles) even when DRT allows auction.

- In some businesses, auction or liquidation may not yield the best return for the banks (e.g. hotel resort in remote area, where no other buyers are keen to spend high amount). Instead if the loans were restructured, banks could salvage more value. But, SARFAESI act doesn’t permit that. Once case goes in the SARFAESI-DRT, there is no scope for arbitration (मांडवाल मुश्किल हो जाती है).

- This is same like, IF Sanjay Dutt was arrested for murdering Fracture Pandya’s brother, the court will only hear case under IPC- whether it was a murder in self-defense or not? But what if both parties went to an arbitrator Suleman Bhai, where Sanjay Dutt would pay blood-money to Fracture Pandya, and all will be forgotten and forgiven? I&B code works on similar principle.

I&B Mechanism

- Company defaults on a loan of ₹ 1 lakh or more.

- Creditors approach national company law tribunal (NCLT), to initiate proceedings under the insolvency and bankruptcy code.

- NCLT will grant moratorium of 180 days (so that no other creditor can unilaterialy attach assets under SARFAESI Act).

- Within that 180 days, an insolvency professional (IP) will make a resolution plan e.g. client should repay only 8 lakhs instead of 10 lakh, loan interest reduced from 18% to 12%, loan tenure extended from 10 years to 12 years or IP could even find another investor to finance the pending project et cetera.

- If 75% of the creditors agree with above resolution plan, then it will be set in motion, otherwise, IP will liquidate the assets of client and recover the dues.

- Client (individual / partnership firm) can appeal against above at the debt recovery tribunals of the SARFAESI Act.

- Client (companies) can appeal against above at the NCLT of the companies Act.

INSOLVENCY AND BANKRUPTCY BOARD OF INDIA (IBBI)

- It is the statutory body that monitors and implements I&B Code.

- IBBI composition: one chairman (M.S.Sahoo), 1 nominated member from RBI, other members from Government’s side. Total 1 chairman + 9 member = 10 people.

- IBBI’s administrative control rests with the Ministry of corporate affairs (MCA). Minister of corporate affairs administers the oath of IBBI chairman.

- Chairman has 5 years / 65 age tenure, whichever earlier. He is also eligible for a reappointment.

- Since IBBI can’t certify / regulate individual insolvency professionals (IP), it delegates this work to Insolvency Professionals Agencies (IPAs). At present three organisations are granted the “IPA” status: 1) ICAI 2) ICSI and 3) Institute of cost accountants

- If IBBI itself launched a database portal to moniter all loans, it’ll be expensive. So, IBBI delegates this work to information utility (IU). In 2017, NeSL: national e-governance services Ltd (owned by consortium of SBI, LIC etc.) was the first to get the IU status.

- It is compulsory for the lenders to share data with IU.

- IU is like Wikipedia of all financial data – borrowing, default and collateral securities. This “Wikipedia” helps in two ways:

- by looking @client’s borrowing history, lenders can make informed decisions about whether to give loan or not and how much interest to charge?

- This database also helps establishing documentary proofs during NCLT / DRT / liquidation- claim proceedings.

(MCQ- Yearbook) Which of the following statutory bodies fall under the Administrative control of Ministry of Corporate Affairs?

- Competition commission of India

- Insolvency and Bankruptcy board of India

- Both 1 and 2

- Neither 1 nor 2

Ans. both fall under MCA.

I&B code vs. SARFAESI liquidation

- by default, I&B code is applicable to all persons and companies EXCEPT

- willful defaulters: A borrower who has the capacity to repay, but he’s not repaying the loan.

- Incapable defaulter: A borrower whose account is in NPA for more than a year, and he has no the capacity to repay even partial loan amount. [एसा नंगा नहायेगा क्या और निचोडेगा क्या?…इसलिए उसकी मांडवाली नही हो सकती.]

- Above two categories of borrowers are not eligible for I&B. Their assets will be directly liquidated under SARFAESI. [क्योकि लातो के भुत बातो से नही मानते]

Banking Regulation (Amendment) Ordinance, May 2017

- I&B can begin against a company only AFTER the bank / NBFC file a motion at NCLT.

- But, public sector bank officials fear media, CBI, CVC, CAG that If corporate loan was restructured, then someone will create controversy, and their promotion will be affected negatively. Therefore,

- PSBs were reluctant/hesitant to even file motion @NCLT. Resolution plan बनवाना तो दूर की बात है.

- Resolution plan can work only if 75% creditors approved. But even in such joint lenders’ forum, PSB-executives will shy away from voting positively.

- To solve this, government drafted banking regulation Ordinance (2017-May).

- Under this ordinance, RBI’s powers enhanced under Banking Regulation Act’49. Accordingly,

- RBI can force the bank file motion @NCLT to begin proceedings under I&B code.

- Voting process tweaked so minority bank-lenders can’t disrupt things. They’ll be bound by the majority decision.

- Once resolution plan is approved, individual bank can’t impose additional conditions. [i.e. If Fracture Pandya & family agreed to Suleman Bhai’s bloodmoney proposal, then, later on Fracture Pandya can’t insist that Sanjay Dutt must also construct a Sangam-age-walla “hero-stone” for his deceased brother.]

Latest economic survey (ES18) proved with data tables that:

- Thanks to I&B code, Banks are able to recover more amount, than If the same company’s assets were auctioned off under SARFAESI act.

- Thanks to Banking ordinance, RBI forced the PSBs to refer ~3 lakh crore worth cases to NCLT for I&B resolution.

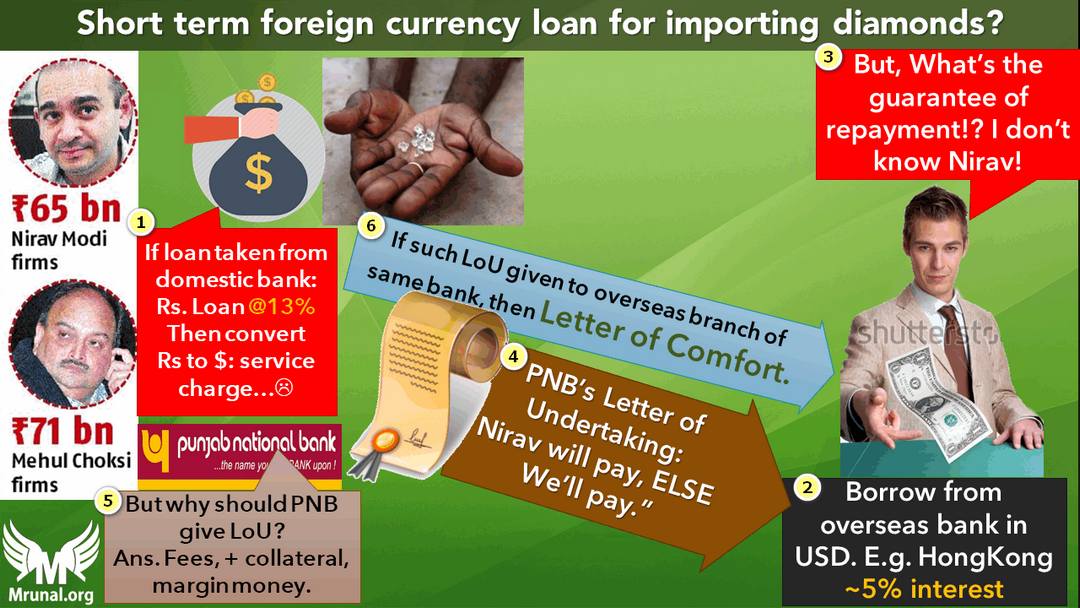

PNB Scam: LoU & SWIFT

What is letter of undertaking (LoU)?

- Suppose, Nirav Modi wants short term loan in dollar currency to import diamonds

- If he borrows from PNB (India), then he has to bear A) higher interest rates (~12%) B) additional cost of converting rupees into dollars.

- But, if he borrows from a bank in Hongkong, then A) lower interest rate (5%) B) those banks directly give loans in US dollars.

- But, the Hongkong Banker may not give such loan to Nirav, because he doesn’t know NIRAV’s history. So, Nirav will have to bring a character certificate / guarentator.

- So, he would get a Letter of undertaking (LoU) from PNB that “if Nirav doesn’t pay your Hongkong loan, we’ll repay that loan.”

- Question: Why would PNB act as ‘big brother’ for Nirav? Ans. Because PNB will charge fees for generating such LoU. PNB could also ask Nirav to deposit some collateral money / diamonds to ensure that even if Nirav flees away, PNB will not make a substantial loss.

- Upon receiving such LoU, the Hongkong bank will create a NOSTRO account for PNB, and deposit loan money in it. From there, PNB will grant authorization to Nirav to use the money for diamond imports.

- If such LoU is generated for the same bank’s overseas branch, then it’s called Letter of Comfort. e.g. PNB (India) generating such letter for PNB(HongKong branch)

How did PNB scam happen?

- Corrupt PNB officer “Shetty” generated LoUs for diamond merchants without taking collaterals.

- Such LoUs were given to Hongkong branches of Axis bank, Union Bank of India, Allahabad Bank and Axis Bank. (As such, non-Indian banks usually don’t accept LoUs. But, Indian banks’ overseas branches accept them, because they want to earn interest.)

- PNB officer Shetty even shared the username/password of PNB’s SWIFT messaging system, so diamond merchants could generate LoUs as and when they pleased. New LoUs were generated to repay old LoUs.

- PNB’s SWIFT messaging system was not integrated with PNB’s core banking solution (CBS) portal, so other officials couldn’t sniff this.

- Scam ran for 7 years, worth nearly 12,000 crores.

PS: Scam’s Modus Operandi not important for MCQs or descriptive questions.

Financial messaging systems

(Mock MCQ) Which of the following is not a financial messaging system?

- NOSTRO

- SWIFT

- SFMS

- None of the above

(Mock MCQ) Which of the following involves three parties?

- Letter of undertaking

- Cheque

- Promissory Note

- All of them

h/ Cheque has three parties: 1) drawer (maker) 2) drawee (bank) 3) payee (recipient.). Promissory note has only two parties: Drawer and payee. LoU has eight parties: 1) opener 2) issuing bank 3) advising bank 4) nominating bank 5) confirming bank .. anyways, such B.Com type MCQs not important for UPSC prelims.

Action taken after PNB fraud

- RBI ordered all banks to integrate their swift messaging system with their CBS system.

- RBI has banned Letter of undertakings (LoU). Consequently, genuine diamond traders are hurt, because they cannot get short term dollar loans from the banks for importing diamonds. In this context, latest economic survey’s observations are relevant: “We should avoid “STICK” policy. Instead, We should use calibrated actions, rather than blunt instruments such as bans, quantitative restrictions, stock limits, and closing down of markets.”

- RBI governor lamented that, “I do not enjoy full independence under the banking regulation act. Because public sector banks (PSB)s are given some exemptions. E.g Under SBI act, only government of India can wind up SBI. Selection and tenure process of the PSB’s higher officials is in control of Government. And soon… इसलिए मुज मे इतना दम नही है की मै कुछ कर सकू. मै RBI का जूनियर मनमोहन सिंह हु.”

- Then CEA Arvind S. criticised RBI governor that “Independence is not acquired through the law but a large part is acquired through reputation and the history of good and effective decision-making.“ This quotation is useful for Mains Gen studies paper 4. (GSM4)

Public credit registry (PCR)

- If RBI maintain a loan-database, then it will reduce the information asymmetry between the borrower and the lender i.e. lenders could know the full history of borrower, his assets and past track record. Accordingly, lender can decide whether to pass his loan application or charge higher interest?

- RBI can use such loan database and its big-data analytics to check the efficacy of its monetary policy and tweak repo rate etc. accordingly.

- To set up such public credit registry (PCR), RBI constituted Yeshwant M. Deosthalee Committee (August 2017 to April 2018).

But why do we need PCR? Isn’t existing mechanism sufficient?

- RBI has given license to four CICs- CIBIL, Equifax, Experian, CRIF Highmark- Under the Credit Information Companies Regulation Act (CICRA 2005).

- RBI has its own “Central Repository of Information on Large Credits (CRILC)” for Loans above Rs 5 cr. Lenders have to submit weekly updates.

- Insolvency and bankruptcy board of India (IBBI) has authorized the National e-governance services Ltd (NeSL) to act as an information utility (IU).

But,

- Not all of these databases are under the direct control of RBI.

- Not all of these databases are covering both individual and corporate borrowers.

- None of these database covers each and every borrower of India.

If RBI sets up its own PCR registry, it can solve above three problems.

(Mock MCQ) What is the objective behind creating a “Public credit registry” in India?

- Dept of Financial Services to have data related to PM-Jandhan overdrafts & farm loans.

- SC directive so that ordinary citizens can know which corporate has borrowed how much from the banks.

- RBI vision to remove information asymmetry between lender and borrower.

- None of the above.

Legal Entity Identifier (LEI)

- if a company is blacklisted by Indian banks, it could apply for loans overseas, and those foreign bankers may not be aware of company’s history.

- So, there should be a global “Aadhar card” number for companies, and they must be forced to quote that number during every financial transaction.

- This is the concept behind legal entity identifier (LEI). It is a 20 digit alphanumeric code for the companies.

- After sub-prime crisis and global financial crisis (GFC), G20 and Financial Stability Board (FSB) came up with this idea of LEI.

- LEI’s Global Boss: Global Legal Entity Identifier Foundation (GLEIF), Frankfurt, Germany

- LEI’s Indian agent: clearing Corporation of India.

RBI’s directives about LEI:

- Companies who have taken loans above Rs.1,000 crore from India banks have to obtain this number by 31/8/2018, then gradually smaller companies have to obtain LEI-number in a phase-wise manner.

- Companies have to quote this number in derivative market as well. (with caveats, not important for UPSC).

- RBI has power to issue such directives under: Payment and Settlement Systems Act, 2007 & Banking Regulation Act’49

(Mock Question) Which of the following organization has mandated Indian corporates to obtain Legal Entity Identifier (LEI)?

- Ministry of Corporate Affairs

- Ministry of law

- SEBI

- RBI

FRDI bill

| Problem: WHAT IF.. | Who will solve? |

|---|---|

| Insurance company itself fails to honor its financial obligations towards the policy-holders? |

|

| What if a company fails to honor its financial obligations? |

|

| Bank itself fails to honor its financial obligations towards the depositors? |

|

What is DICGCI?

- Deposit insurance and credit guarantee Corporation Act 1961: mandates that all banks have to buy insurance on their deposit accounts (current account, savings account, fixed deposit etc. all types of accounts)

- It means the banks have to pay insurance premium to the DICGCI.

- DICGCI is 100% owned by the RBI. One of RBI Deputy Governor acts as chairman of DICGCI. Its HQ is in Mumbai.

- When the bank shuts down, DICGCI will pay upto Rs. 1 lakh insurance to every deposit holder. If you had deposited more than 1 lakh rupees in a bank, then you’ve to wait till RBI / cooperative registrar liquidates the bank to give you remaining money (fully or partially)

If there is DICGCI, then why FRDI bill?

- DICGCI covers only banks. It doesn’t cover NBFCs. [Non-banking financial companies such as mutual funds, investment funds etc.]

- 2002: UTI (a Government owned mutual fund company) made big losses. DICGCI not liable to protect its depositors. So, Government had to give Rs. 14,561 crores bailout package.

- Under Banking regulation Act, RBI can do only two things: 1) merge weak bank with strong bank 2) liquidate the weak bank. It doesn’t have other resolution instruments. Adding insult to injury, RBI doesn’t have monopoly of control over cooperative banks- their final liquidation process rests with the registrar of cooperatives. For example,

- 2001: Share broker Ketan Parek swindled Madhavpura cooperative banks’ Rs.1,200 crores. DICGCI paid only Rs.464 crores to depositors. [Because its maximum guarantee is Rs. One lakh per customers]. To recover the remaining amount, Central Registrar of cooperatives (under Agri. Ministry) appointed a “liquidator” under Multi-State cooperative societies Act. But, Ketan Parek obtained SC stay order till 2017. So, 1200 – 464 = 736 crore of bank depositors’ money still stuck.

- Under SBI act, only government of India can windup SBI. In future, if SBI depositors’ money stuck, and new government is running with support of Leftist parties, then it may not take fast decision to liquidate SBI (due to Bank labour union!)

- Means, the present DICGCI model is insufficient to protect even bank-depositors.

FSLRC commission

- 2011-13: Financial Sector Legislative Reform Commission (FSLRC) under Justice BN Sri Krishna.

- He observed that it’s neither feasible nor desirable to have 100% failure prevention of financial intermediaries (FI = banks and non-banks).

- If an FI fails, that’s also a good thing because its labour and capital can be shifted to more efficient firms. But we must resolve this swiftly, else investors, depositors and citizens at large will suffer.

- Therefore, we should convert DICGCI into a resolution corporation (RC) for both banks and non-banking financial intermediaries, through a law- just like the advanced economies (AE) of the world.

- 2017, August: Government drafted Financial Resolution and Deposit Insurance (FRDI) Bill, 2017 to implement above suggestion.

FRDI bill: Salient features

- It transforms the DICGCI into a Resolution Corporation (RC).

- All financial intermediaries (banks and NBFCs) will have to buy insurance from RC, to protect their depositors.

- RC will monitor and classify these banks and NBFCs into following risk categories: Low, Moderate, Material, Imminent, Critical.

- When a bank / NBFC comes in ‘imminent risk’, RC will draft a resolution plan before it reaches critical risk.

- RC could workout following type of resolutions:

Resolution Tools against weak FI

| Sale / Merger | With another financial intermediary (FI). This will ensure continuity of services for the customers. (e.g. if PNB merged with SBI; UTI-MF merged with Reliance-MF) |

| Bridge institution | If RC is unable to find a merger-worthy FI immediately, then RC will create a new company to look after the affairs of the sick-FI, until a suitable buyer is found. |

| partially sell-off assets | In some scenarios |

| Liquidation | In the worst case scenario. |

| Bail in provisions | In some scenarios. |

What is Bail-In and Bail-Out?

Usually a financial intermediary (bank, insurance company, mutual fund) runs with following equation:

| Capital | + liability = | Assets |

|

|

|

Crisis comes when right hand side of equation becomes weaker and it can’t balance the left hand side.

- PNB runs into huge NPAs vs. Depositor wants Rs.5 lakhs back.

- Resolution corporation will pay the depositor Rs.1 lakh. He still wants 5-1 = 4 lakhs back.

- If Government of India injected additional capital into PNB, and from that money, if Rs.4 lakhs were given to depositor = “BAIL-OUT” using tax payer’s money.

BUT instead, what IF Resolution corporation takes following action?

- RC orders PNB to sell off some of its assets and repay Rs.3 lakhs (instead of 4 lakh) to the depositors, and then continue operations. (= liability reduced)

- RC merges PNB with SBI. PNB depositors’ bank account will be shifted to SBI, but there it only shows Rs. 3 lakh in his account? (= liability reduced)

- OR RC creates a “bridge company” and handovers PNB’s ownership and management to that Bridge company. And that Bridge company’s shares with face value of Rs. 3 lakh are given to the depositors, instead of giving direct money. Later, depositor can sell his shares to other party OR wait for the bridge company to revive PNB’s business, then he’ll get dividend from the profit of this revived PNB under new management. (= liability is restructured and reduced)

So, when depositors’ liability is restructured / reduced to save the financial intermediary… it is called “Bail-In”.

Why “Bail-in” fear is wrong?

- Even under the Banking regulation act 1949, when RBI forces the merger of weak bank with strong bank, it could reduce liability of depositors when accounts are shifted to the new bank. So, Bail-in is not a new idea.

- Just like DICGCI, the new RC will be insuring Rs.1 lakh rupees for every depositor. (or more, if parliament increases the limit).

- If depositors feel injustice in Bail-in, they can file claim at National Company law tribunal (NCLT) for higher compensation.

- Public sector banks are not sacred cows. It’s not written in the FRDI bill that PSBs can’t be shutdown and liquidated. So, the fears that PNB’s losses will be offset using depositor’s money… is a baseless fear.

- RC will have to send report to Union government and the relevant financial regulator (RBI, SEBI etc) to justify why “Bail-in” provision was used in a particular case.

- Bail-in is a “prospective” provision applicable on future deposits & investment. It can’t be applied “retrospectively” on past-deposits to pay-off the past scams like Nirav Modi and Vijay Mallaya.

Next article?

- 2.11 lakh crore recapitalization package for BASEL-III, 1.35 lakh crore worth Bank recapitalization bonds, and EASE-Framework for reforming public sector banks.

![[Win23] Economy Pill4ABC: Sectors: Agri, Mfg, Services, EoD, IPR related annual current updates for UPSC by Mrunal Patel](https://mrunal.org/wp-content/uploads/2023/04/win234b-500x383.jpeg)

u are like father and mother to us :). who take cares of their child and spoon feeds him the needs.

sir! are you not going to upload economy lectures this session? please let me know sir.

Thank you, Super Human Mrunal Sir

Thankyou sir.

मृणाल सर जी क्या इसबार आप वीडियो नहीं बनाओगे क्या. अगर आप वीडियो बनाओगे तो बड़ा फायदा होगा. कृपया हम बिहारी लोगो पे एहसान कर दीजियेगा.

i was clueless till i read this article tough i read all current. you should write for THE HINDU (inke specialist ka concept bhut kamzoor hota hai aur humara bhi kar dete hai.)

Thanks so much, Sir. You articles are as good as your videos, and that’s saying something since your videos are the best in the market.

Thank you, sir.

Thank you so much sir! for this valuable article….

Sir you are great

Thank you sir…

Jai Ho Bhai Ki!

Thanks a Lot

Sir how can lenders make informed decision about giving loans to lenders i am not able to understand the process of IU

MRUNAL SIR PLEASE HELP

Mrunal da….gareebo ka maseeha :)

thanks mrunal sir

Thanks a lot

Thank You Sir :)

Shukriya sir, Rabb thonu saariyan khushian bakshe.

Thankyou sir. Appreciate your effort .

I think NPA on 31/12/2017 is 8.40lakhs crores…. Please correct me if am wrong

Yes I think he intended to say 2017 instead of 2018.

Sir i follow many websites for civils but i can confidently say that this is the best one , i have only one request please post atleast 2 articles in a week sir. i want to see your website expand into other domains as well not just economics.

sir, app best ho sir appke you tube per video nahi aye for buget/economic survey

Sir thanks for this efforts for us. But I’m unable to find videos of the same on YouTube. Is these only article / ppts or videos are being uploaded on any other YouTube channel.

Thanks again sir.

Thanks a lot sir helping from the very first day of my preparation.

sir……

in bail-in related articles….

it’s depositors’ liability or bankers’ liability…….?

Sir, I have a query regarding “bail-in” example given by you.

You said that the depsitor initially had 5 lakhs with the Bank and during bail-in clause is invoked, only 3 lakhs were restructured as shares of that Bank. So, where does the remaining 2 lakhs of the depositor gone?

Is it depositor’s liability or bank’s?

About Bail-in.

I thought I understood this perfectly from the news (DIGCI esp.) But mrunal sir never fails to give a new perspective! Thank you so much sir.