- Prologue

- BO1: RRB act

- BO2: Small banks and Payment Banks

- BO3: Kotak-ING Vyasa Merger

- BO4: NBFC regulation guidelines

- BO6: SBI Share splitting

- Mock Questions for Banks Exams

Prologue

- In this article, we’ll checkout a few current developments in Banking sector at “Organizational” level.

- In the next article, we’ll see developments at “operation / product” level e.g. Bharatiya Bill Payment system, SBI’s Shariya fund, E-mandate etc.

- Utility: Mainly for bank interviews and MCQs.

BO1: RRB act

Background theory

- 1976: Regional Rural banks Act, based on Narsimhan Committee’s recommendations for greater financial inclusion.

- RRBs aim to combine efficiency of a commercial bank with grassroot networking of a cooperative society.

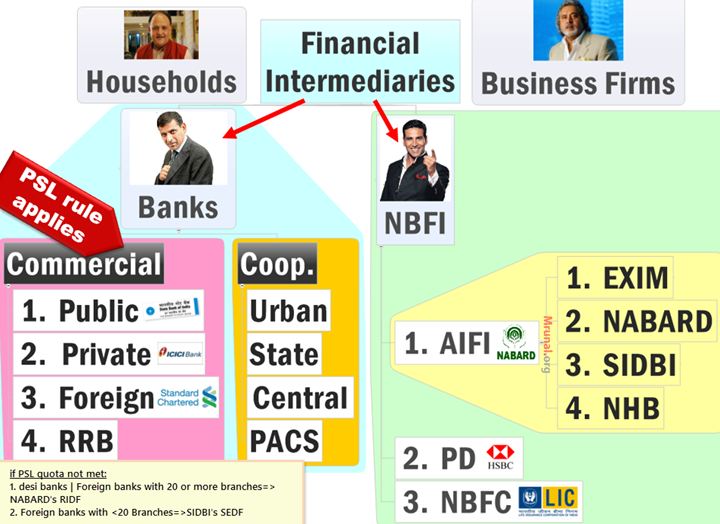

- RRB is one type of Commercial bank. Therefore, it has to comply with RBI’s SLR, CRR and PSL requirements (Priority sector lending).

- Sponsor bank helps the RRB in HRM-training, account keeping services.

Anyways, RRB is an old theory topic, why has it resurfaced again?

| RRB Act 1976 | RRB Amendment Bill 2014 |

|---|---|

|

|

Shareholding

|

|

| State government’s shareholding was fixed to 15% | States can buy more shares, to increase their shareholding above 15% |

| — | RRB can appoint Board of directors from outside union-state and sponsor bank nominated people. |

| — | One person cannot become director in 2 RRBs. |

| Director’s tenure limit: 2 years | 3 years |

| — | Person cannot remain director for more than 6 years. (Meaning one individual can be an RRB director for only two terms 3 + 3.) |

AIFI: All India financial institutions, PD: Primary Dealers

BO2: Small banks and Payment Banks

| 1998 | Narsimhan-II Committee recommends small banks in India. |

|---|---|

| 2009 | Raghuram Rajan Committee says the same. |

| 2013-14 | For greater financial inclusion, RBI’s Nachiket Mor Committee had recommend new types of banks such as payment banks and wholesale banks. |

| 2014, Feb-March | Bimal Jalan Committee approved Bandhan Microfinance and IDFC for opening private commercial banks. Bimal too recommended RBI to permit ‘differentiated’ banks in India. |

| 2014, Nov | Rajanbhai invites applications for Small banks and payment banks. |

Common Features of Small bank and Payment banks

- Deadline to apply for License: 16/01/2015. After that, an external screening Committee will decide the winners, probably in July 2015.

- Minimum capital requirement to apply for license: 100 crores. (For commercial bank license, it was Rs.500 crores)

- They’ll have to comply with the FDI norms like regular commercial banks i.e. 74% FDI only.

| Small banks | Payment banks |

|---|---|

| Can accept all types of deposits like a commercial bank (CASA, FDRD etc.) |

|

|

|

| Target customers: MSME businessmen, unorganized workers, small and marginal farmers. | Target customers: poor, migrants, unorganized workers wanting to send remittances home. |

| Focus: Deposit and loans | Focus: Payment/remittances only. Including cross-border remittances. |

Who can apply?

|

Who can apply?

|

Conditions:

|

Condition:

|

- Remaining differences are of technical nature like tier-1 capital etc. not worth the effort for MCQs.

- Public sector bank employee union has opposed this move, saying existing public sector banks are capable of delivering these services and last mile financial inclusion.

BO3: Kotak-ING Vyasa Merger

Kotak ING Vyasa Merger

RBI, CCI and other financial regulators have approved the ING-Vysya Bank to merge with Kotak Mahindra bank (2014, November).

| Kotak Mahindra | ING Vysya bank |

|---|---|

| Got Banking license in 2003 |

|

| 4th Largest private bank | 7th |

| Founder: Uday Kotak |

|

After Merger

|

After merger,

|

- Ranking of private Indian banks after this merger: (1) HDFC (2) ICICI (3) Axis (4) Kotak.

- Kotak group also got “in-principal” approval to takeover general insurance business from ING-Vysya.

BO4: NBFC regulation guidelines

Background

- Non-banking financial companies serve as an important tool for financial inclusion and turning savings into investment.

- But, in the 90s, Harshad Mehta and other scams put all Non-banking financial companies into bad light.

- As a result, RBI and Government always adopted precautionary and sometimes ‘step-motherly’ regulations on NBFCs. For example- they’re not allowed to get tax-benefits on NPA, mosto f them forbidden from external commercial borrowing (ECB), they are not given loan recovery powers under SARFAESI Act and so on.

- 2014, November: Finally, Rajanbhai decided to empower NBFCs, on par with Commercial Banks.

RBI’s new guidelines for NBFCs:

[no *that* important for MCQs, just memorize a few points for interview]

- Fair practice code (FPC) and Know your customer norms (KYC) will not apply to an NBFC IF

- Its asset size is less than Rs.500 crore AND

- It doesn’t accept deposits from public AND

- It doesn’t have any customer interface.

| 2014 |

|

|---|---|

| 2016 |

|

| 2017 |

|

| 2018 |

|

| Not done |

Allowing NBFCs to use SARFAESI Act powers to teach lessons to loan-defaulters. [Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act] |

BO6: SBI Share splitting

- Earlier: ICICI and PNB announced share splits- One share divided into five.

- SBI announced 1:10 share split in 2014, November. Meaning, you’ll get 10 shares of SBI, for every exiting 1 share owned by you.

| Before | 1 share with Face value of Rs.10 |

|---|---|

| After | 10 shares with face value of Rs.1 |

Benefits of share-splitting?

- Increases in share-quantity, thereby increases the participation of Retail investors- like cutting one banana and selling five of its pieces.

- Provides liquidity to investor. Example, if you had 1 share of infosys worth Rs.1 lakh, it’ll be difficult to find a buyer.

- But if you had 1000 shares of infosys worth 100 rupees, easier to find a few buyers interested for purchasing 20-30 shares individually.

- Thus share-splitting increases “demand” and new investors. Hence P/E Ratio also improves. [Share Price to earnings ratio.]

- Share splitting or stock splitting, doesn’t change following

- Company’s value. because Total face-value wise, 1 share x Rs.1 lakh = 1000 share x 100 rupees.

- Company’s market capitalization. For the same reason given above.

Mock Questions for Banks Exams

[columnize]

Q1. Consider following statements about RRBs

- RRBs are jointly owned by Government of India, the concerned State Government and Sponsor Banks

- In RRB, the sponsor bank is the majority shareholder.

- Both A and B

- Neither A nor B

Q2. The RRB Amendment Bill 2014

- Provides flexibility to shareholding pattern of Union, states and sponsor banks.

- Increases authorized capital of RRBs.

- Permits Individual to hold board directorship in multiple RRBs

Correct statements are

- Only 1 and 2

- Only 2 and 3

- Only 1 and 3

- None of them

Q3. If an RRB has failed to fulfill its PSL quota for the given year, then it’ll be required to submit money to ____.

- NABARD’s RIDF

- SIDBI’s RIDF

- NABARD’s SEDF

- None of above.

Q4. Which of the following is/are example(s) of Differentiated banks in India?

- Small banks

- RRBs

- Payment Banks

Answer choices

- Only 1 and 2

- Only 2 and 3

- Only 1 and 3

- All of them

Q5. Minimum capital required to apply for license of small bank / payment bank is ____.?

- 100 crores

- 200 crores

- 500 crores

- 1000 crores

Q6. Who among the following is/are eligible for applying small bank license?

- An individual with experience in cooperative or banking sector

- Corporate houses

- Non-Banking financial companies

Answer choices

- Only 1 and 2

- Only 2 and 3

- Only 1 and 3

- All of them

Q7. Which of the following features are not available at a Payment Bank?

- Getting housing loans

- Getting a Credit card

- Opening a current account.

Answer choices

- Only 1 and 2

- Only 2 and 3

- Only 1 and 3

- All of them

Q8. Who among the following, can open an account in Small bank?

- NRI

- High net worth individual

- Migrant laborer

Answer choices

- Only 1 and 2

- Only 2 and 3

- only 3

- All of them

Q9. A Payment bank will have to fulfill which of the following condition?

- 40% of the loans must be given under priority sector lending (PSL)

- 25% of the NDTL must be invested in G-sec.

- Maximum balance per client cannot exceed Rs.50,000

- None of above.

Q10. Which of the following mergers took place in 2014-15?

- Benares State bank with BoB

- Bank of Madura with ICICI

- ING Vysya with Kotak-Mahindra

Answer choices

- Only 1 and 2

- Only 2 and 3

- only 3

- All of them

Q11. Arrange the following banks in descending order of their total-assets?

- Kotak-Mahindra

- Axis

- ICICI

- HDFC

Answer choices

- 1234

- 4321

- 1243

- 2134

Q12. How does an investor benefit from Stock-splitting?

- It increases market capitalization of the said company.

- It decreases the liquidity of stocks held by him

- It increases the dividend earned by him

Answer choices

- Only 1 and 2

- Only 2 and 3

- Only 1 and 3

- None of them.

Interview

- What do you know about RRB Amendment bill? How will it benefit Indian economy?

- What are your views on consolidation of Public sector banks in India?

[/columnize]

Visit Mrunal.org/Banking for more articles related to Banking, Finance and Insurance.

![[Win23] Economy Pill4ABC: Sectors: Agri, Mfg, Services, EoD, IPR related annual current updates for UPSC by Mrunal Patel](https://mrunal.org/wp-content/uploads/2023/04/win234b-500x383.jpeg)

such a catchy and funny cover..:P :v :D

thanx fr d article MrunalDa…:)

@Kuku_Dhakkan The cover is funny but saddest part is that it is true.

Almost 10 lakh students are giving UPSC of which atleast 1 lakh are full timers. In next 5 years hardly 5000 will get in. What about the rest? Some will get in SSC, Bank PO etc… Others who could not get any post in any competitive exam would have definitely wasted their ‘jawani’ . Whether you like it or not the ‘knowledge’ that we get i.e. history, geography etc… is useless in the outside world.

The huge number of attempts limits and high age limit given by UPSC and other competitive exams has ruined many lives. I think it is best to have a self defined attempt limit (especially for full timers) to avoid wasting our ‘jawani’ . After crossing this limit, leave UPSC, SSC etc… and try to get a job, any job.

@Sanket

Really boss, you such a pessimistic person. Hats off to you. You are justifying your pessimism with figures………..great boss………….For ur kind information IBPS Clerk(only one of three exams of IBPS ) recruits more than 30 K students every year. UPSC exam is lifestyle kind of exam ……….don’t compare or do anything like analogy with other exams. Get a copy of “Monk who sold his ferrari” and feel the difference and stop discouraging others. There are “innumerable” opportunities in life ……..not just becoming a DC of area or chief secretary bro…………..and then rule like monarchs.

@ I_Have_Many_Dreams Both of us are saying the same thing but still I am a pessimist and you an optimist?

I know about bank exams and I also know that Bank Clerical recruits In large numbers. However if an aspirants is unable to crack UPSC or SSC for many years then s(he) will face problems w.r.t age limit in exams like bank clerical.

That’s the reason why I said that an aspirant(especially full timers) needs to have a self defined attempt limit for UPSC, SSC etc… after which s(he) should start trying for other jobs like Bank clerical. If s(he) is too late, it might happen that s(he) will end up not getting any post(or job) anywhere.

Many toppers had a self defined attempt limit after which they would either leave competitive exams altogether and returned to their old jobs or give some other exam. Thus many avoided wasting their ‘jawani’ in pursuit of exams like UPSC, SSC etc…

#Sanket and #DreamerBoY…:)

both of u are correct and thik h yaar itna heavy exam h toh thoda bht pessimism aa jaata h.. :) ..part of lyf..hm log superman nahi hain naa jo har cheej se har feeling se upar uth jaayenge..:) lekin dekh dost..jo bhi bande UPSC prepration mein entry karte hain naa wo isko as a passion..iski prepration ko as a motivation..booster..and as a real beautifull journey maante hain and dats wht d beauty of UPSC… not mere a job..BUT a DREAM.. so whtever it takes to achieve JUST PUT DAT.. karam karo phal ki chinta mat karo..hai naa..

and @Sanket yaar jaha tk jawani waste krne ki baat h toh UPSC prepration hamare youth lyf ko beautify kartaa h..hehe jawaani barbaad kaekoo hogi isme..haan side by side if anyone feels ki other exams dete rhne chaahiye toh de denaa chahiye… ab dost level of competition bhi toh dekho…those who write mains are elite club and too beat them is a REAL GAME…so just apne weapon ko sharp karo and BANG BANG BANG..! jawaani mein hi UPSC bhi clear hota h dost..jawaani barbaad uski hoti h jo is precious tym ko vyarth kar deta h in all shit and crap wd tom dick harry.. dont b negetive…just keep working towards ur goal wd full dedication..safalta milnaa yaa naa milna depends on HIM..bs aap apna karam aur prayaas imaandaar reh kr kro..

happy studying dosto.. :) shubhaastu panthaan: :)

this is what i call an attitude…dost..UPSC is not end of lyf..its just a passion…mila toh bht badhiya or naa bhi milaa toh bhi hamne UPSC ko jiya..:)

dekh dost jo bhi with dedication mehnat karega toh maan lo UPSC naa huaa tb bhi kuch achchaa milega hi usko..UPSC is top step of stair..ydi wo naa pakad paaye toh at least top 2 ya 3 step jaroor pakad logey…:)

and yaad rkhna dost… history geo pol sc kch bhi padho..this all is your arjit gyaan and knowledge kabhi barbaad nahi jaati..in sum form or other..u will get recognition fr ur knowledge..thik..:)

duniyaa k liye nai apne liye padhnaa h naa..:)

jaha tk self defined attempt ki baat h toh ye to yaar personal choice h sabki…

and upsc mein jawaani barbaad ni hoti balki jawaani sudhar jaati h dost..jawaani toh unki barbaad hoti h jo bas farzi tympaas krte hain..at least hm log apna youth ka precious year apne passion apne dream ko poora karne mein laga rhe hain..hai naa..we r not aimless..so jawaani waste kaise hui? :)

shubaashtu panthaan: happy studying dost… :) kaekoo tension lene kaa… INDIA calling..:)

@Kuku_Dhakkan Well said.

We have changed a lot due to UPSC. We can read a lot faster and understand data much better than earlier. Earlier we used to believe everything we heard or read but now we have learnt to ask the right questions and try to see each issue from different angles and appreciate others perspective.

Of course we should have a back up or a self defined attempt limit. But we should also appreciate this increase in grasping power, memory, logic, maturity etc… due to UPSC. This will definetly translate to success some day or the other.

Besides some day we aspirants are gonna marry and have kids who will go to school and study history, geography etc… Maybe at that time our conceptual clarity in history, geography etc… and the study skills we learnt will come in use for guiding them.

Anyway, you are right. UPSC se jawaani waste nahi hoti balki sudhar jaati hain.

Of course we should have a back up or a self defined attempt limit. But we should also appreciate this increase in grasping power, memory, logic, maturity etc… due to UPSC. This will definetly translate to success some day or the other.

Besides some day we aspirants are gonna marry and have kids who will go to school and study history, geography etc… Maybe at that time our conceptual clarity in history, geography etc… and the study skills we learnt will come in use for guiding them.

bhaai teri is lyn ke liye 100 tho likes..:)

ab cheer maaro and jut jao UPSC 15 mein..kon jaane kya likhaa ho abki baar… :)

@U both

Have we reached anywhere?

Yaar ek positivity hee to hai………what we need ……..knowledge ka bhandar to mrunal sir se bhi mil jata hai………Really

Mrunal sir u r GREAT……..

@sanket @DreamerBoy..

yes we r really no where..but if we keep moving forward wd positivity..we will be somewhere someday.. :)

and MrunalDa is our superman… :)

happy studying to all

True,sheer wastage of human capital

1 c

2 a

3 a

4 c

5 a

6 d

7 d

8 c

9 a

10 c

11 b

12 c

sm answers are wrong according to mrunal sir’s notes

Good one for a quick revision with some new points. Thanks Mrunal :)

Please send me all new topics throuh mail

thanx sir..

Very useful. Thank you.

Regional Rural Banks (Amendment) Bill, 2013 or 2014??????

many places i have seen 2013

Anuj, latest RRB bill is of 2014. See the list of bills presented in Winter session here.

mrunal bhai thaku :) ..keep updating our gs sections with such articles …bas ap aise hi apni kripa hum par bnaye rhe…

Mrunal rocks

AAACACACBCBD

Hey anuj ..well very first RRB maintain the CRR(now question arises that only commercial banks do that then why rrb?) so simple rrb is a type of commercial bank. (explained ahead) when rrb established in 1976 ..it wasn’t commercial at all (so no crr) but there were some reforms taken place in three phases (mainly 2nd phase ) due to which now rrb comes under the category of scheduled commercial banks so (now they maintain CRR) ……

Thank you..Arya..!!

thanks sir

Very useful… Thank you

Sir, NIACL legal specialist exam… Might b conducted on 16 Jan…. And can u plz provide me any link frm wr I get Sm previous years or sample question paper, fr revision.

And wat is the parameter of GA for this exam…. Is thr any difference between this exam and IBPS.

hey Avinash ,,NIACL legal specialist exam was scheduled on 10 n 11th jan , has it been postpond???

Is it important for civils Mrunal sir?

SIR?MAM,

why GST is touted as India’s biggest indirect tax reform since 1947

pls clarify why it needs to be ratified by half of state assemblies as it doesn’t lie under the criteria to seek ratification from state assemblies.

Why deadline of APRIL 2016 is given to GST bill

already this year winter session is over….so discussion on it will takes place..at next year budget session(feb month)…..and since it is a constitunal amnd. bii…..it has to be passed with special majority from both houses and also…ratified by half of the states…then president nod…..and next financial year is starts from…1st april..so it is not possible to implement..it……therefore it is extended to april…2016

Can u plz tell me when will SSC-CGL tier-1 2014 results be declared?

already this year winter session is over….so discussion on it will takes place..at next year budget session(feb month)…..and since it is a constitunal amnd. bii…..it has to be passed with special majority from both houses and also…ratified by half of the states…then president nod…..and next financial year is starts from…1st april..so it is not possible to implement..it……therefore it is extended to april…2016

A small correction Kotak is 4 largest private bank in terms of branches and Federal bank is 4 largest private bank in terms of capital.

sir, please provide the correct answers of these mock questions also

answers of Q-3 , 8 , 9 ?

please can any one explain me about arms trade treaty.. .

….i have read about it frm newspapers.

.but unable to get it properly ..

.n what is india’s stand on it

1. A

2. A

3. A

4. C

5. A

6. C

7. A

8. C

9. A

10. C

11. B

12. C

RRB also a type of differentiated bank

http://www.thehindu.com/opinion/columns/C_R_L__Narasimhan/differentiated-banks-has-their-time-come/article6252844.ece

Sir,

Is business correspondent model(BC) of financial inclusion allowed for both small and payment banks or only for payment banks?

parthi is this you from team work grup?

No sir… I am not from Any team.. Just lonely novice.. Preparing for Civils

all d best dost.. :)

Sir,

Is policy rate(repo and rev repo) applicable for small banks similar to commercial banks?

Correction needed : Kotak Bank- Total branches ~1.2 lakh

Thank for the update …..any one can tell me for economic which artical had to study by mrunal .

Dear mrunal sir.

Please write answers

ANSWERS-

1-A

2-A

3-A

4-C

5-A

6-C

7-A

8-C

9-D

10-C

11-B

12-C