- Why identify banks “Too big Fail”?

- Who will identify D-SIB?

- D-SIB in India

- Benefits of D-SIB norms?

- Limitations of D-SIB norms?

- Mock questions

Why identify banks “Too big Fail”?

- 2009: Financial stability board (FSB) was setup. It is an international body affiliated with G20. Purpose: Monitor Global financial system. HQ: Basel, Switzerland.

- 2010: FSB observes following:

- Each country has certain “big” banks with huge client base, commanding billions of dollars, run cross-border and cross-sector (insurance | pension etc) investment through their NBFCs. (Non-banking financial companies)

- These NBFCs act as “shadow banks”, because while they carry bank like operations but not subject to bank like regulations.

- If the parent banks fail, Government is forced to ‘rescue’ them with ‘bailout package’ to ensure that national economy doesn’t collapse and ordinary citizen-clients don’t suffer. E.g. Subprime crisis, US & UK Government had to spend billions of tax-payer money to rescue their large banks.

- Consequently, these banks become confident they’re “too big to fail” so they will always be rescued by market-forces or the government, will continue to indulge in grey-areas and reckless practices.

- Hence, we need to identify such systematically important banks (SIB) at Domestic and global level.

- We must force them to have additional capital/backup against financial emergency, so that taxpayer money not wasted in rescuing them during crisis.

D-SIB in India

- 2014: RBI issued guidelines for Domestic Systemically Important Banks (D-SIBs).

- Each year in August, RBI will disclose the names of banks designated as D-SIBs, using two-step technical process that is not important for ordinary exams except may be for RBI Grade “B” office interviews.

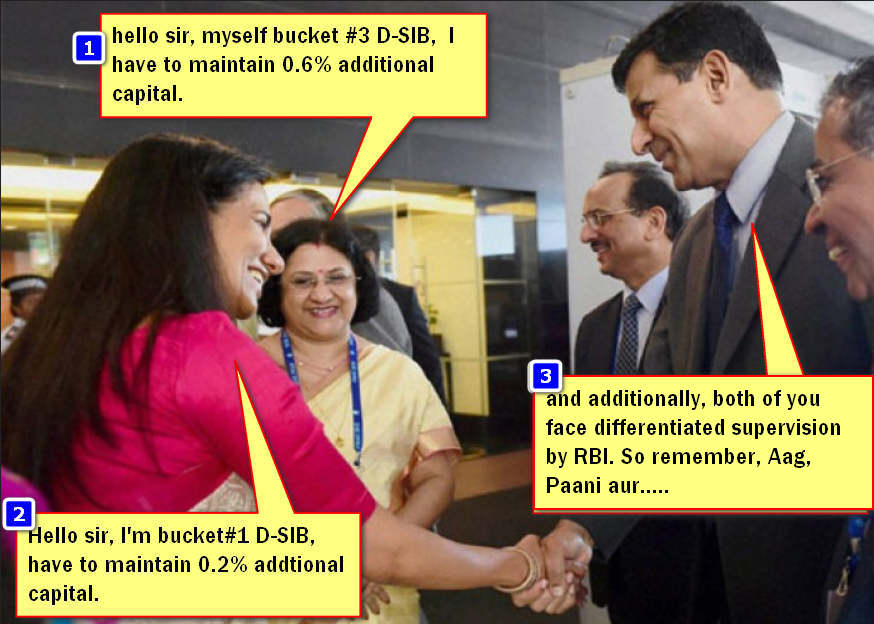

- Further, these D-SIBs are sub-classified into bucket number 1 to bucket number 5 depending on their size (as % of GDP). Higher the bucket number, more capital they’ve to maintain.

- 2015: SBI (Bucket 3) and ICICI (bucket 1) declared as D-SIBs. List will be updated each year in August.

| Bucket | Domestic Systematic important Bank (D-SIB) |

Additional Capital requirement |

|---|---|---|

| 5 | None for now | X + (1.0% of risk weighed assets RWAs) |

| 4 | None for now | X + (0.8% of risk weighed assets RWAs) |

| 3 | SBI (D-SIB) | X + (0.6% of risk weighed assets RWAs) |

| 2 | None for now | X + (0.4% of risk weighed assets RWAs) |

| 1 | ICICI (D-SIB) | X + (0.2% of risk weighed assets RWAs) so if they had to set aside Rs.1 earlier, now they’ll have to set aside Rs.1.02 |

| — | Ordinary bank | Suppose they’ve to maintain “X” crores in tier-1 common equity in BASEL norms |

- ICICI says they already maintain 12% above tier 1 so no problem for them to comply with this D-SIB game.

- But, SBI says they’ll have difficulty in arranging this much capital and hoping Government of India will help.

Benefits of D-SIB norms?

- 2013: Cobrapost sting operation caught ICICI indulged in money laundering and KYC-Violation, RBI had imposed Rs. 1 crore fine.

- Now that ICICI is classified as a D-SIB, Rajan Bhai will put stringent supervision over it, this will prevent ICICI/SBI from indulging in any grey areas, knowing well what happens when anyone tries to play with Aag (fire), Paani (Water) and rajanbhai.

- If such large banks behavior in prudent manner, it’ll prevent any national financial crisis in the first place.

- Even if financial crisis happens, SBI and ICICI will be able to run their operations, because of the additional capital.

- Government of India won’t have to use tax-payer’s money to rescue them.

Limitations of D-SIB norms?

- D-SIB mechanism alone not sufficient for preventing banking sector collapse, because apart from D-SIB, we must also control their “shadow bank” children.

- UK introduced a “ring fencing” law i.e. banks need to strictly separate operations from the NBFCs owned by them. In India, although we’ve RBI-guidelines for this but much needs to be done, e.g. Implement Justice BN Srikrishna’s report for financial sector legislative reforms (FSLRC), create new single statutory bodies to have overall supervision of sharemarket-insurancemarket-commoditymarket-pensionmarket and so on.

- 2014: News reports hinted that RBI was going to list 6 banks as D-SIB (viz. SBI, PNB, Citi, Standard Chartered, ICICI and HDFC). But the official list released in 2015 contains only two banks. The other four (PNB, Citi, Standard Chartered and HDFC) are also ‘too big to fail’ and should have been included in this list.

- In other nations, D-SIBs are required to maintain upto 3.5% additional capital. In India, highest Is just 1% (for D-SIB in Bucket#5) So, RBI’s norms are not as stringent as in other countries.

- Counter argument: Each central bank free to decide formulas and parameters. Given Indian economy’s size and otherwise strict regulation of banking sector, the current formula is sufficient.

Mock questions

Q1. A Domestic Systemically Important Bank (D-SIB)

- Has to maintain additional SLR and SLR

- Has to follow separate norms for priority sector lending.

- Has to invest additional money in compulsorily in G-Sec

- None of above

Q2. The concept of “Domestic Systemically Important Banks (D-SIB)” is the brain child of __.

- US federal reserve

- FSB

- Basel Committee on banking supervision

- Justice BN Srikrishna commission.

Q3. Consider following statements about Domestic Systemically Important Bank (D-SIB)

- A D-SIB is required to maintain two banking ombudsman per state.

- The Chairman/CMD of a D-SIB will be selected and appointed by a Committee made up of RBI governor and representatives from Union Government.

- Both A and B

- Neither A nor B

Q4. Many Factual MCQs possible from “bucket” table of above article. They’re important for Banking exams but not for UPSC.

Mains-Descriptive Question: As such this is technical topic, so direct question seems unlikely in UPSC Mains but it becomes a fodder point in the larger generic /vague question about controlling / reforming the banking sector / financial sector.

Interview: What is D-SIB, what is Shadow bank, How do they pose challenge to an Economy, what steps are done at national and international level to control them? What more should be done in your opinion?

![[Win23] Economy Pill4ABC: Sectors: Agri, Mfg, Services, EoD, IPR related annual current updates for UPSC by Mrunal Patel](https://mrunal.org/wp-content/uploads/2023/04/win234b-500x383.jpeg)

D,B,D

1-D

2-B

3-D

thank u mrunal sir for this beautiful articles……eagerly waiting for another article…..pls post it very soon…

regards

subhash

Sir it will be very helpful if you write an article on Chinese economy crisis …

Watch Policy Watch on Youtube Channel of Rajya sabha TV. They have explained it in detail . It has also been covered briefly in “The Big Picture” on the same channel.

Sir u r a messiah for those who cannot afford coaching plz continue writing such wonderfull articles

Thanks sir for providing current informative of banking.

guys my cutoff is 108 as per shankar key SC category will I get chance to write Mains BOTH IAS & IFoS ???

Thanx a lot Sir for the above article….

Mrunal Sir. Feels so nice to read your humour filled and informative articles. I know you have a life of your own but please take out some time to help us with Mains’15.

(Wo kya hai ki aur kisi ka padhaya economics ab jamta nahi aur bheje me ghusta nahi. Hehe)

thanx for coming again sir :) China and international currency devolution and currency war.. please enlighten about that sir..

Happy to see you again, sir. Please, write on some burning issues important for mains 2015.

Thank you.

thanku sir…. great work

Bonanza of learnings with fun continues…Welcome back Sir!!! Expecting some decent sixes i.e Some questions with model Answers.

1) D

2)B

3)D

Thank you sir for this useful article.

Thank you sir for your hard work.

O boss o sir jiii. life ruki pdi h… plz send us analysis of paper 1 prelim….i need it badly

Much needed. Sir please continue these adds a lot values.

Thanks, Mrunal bhai, got almost all of the economy questions in CSAT paper 1 because of your economy lectures, great work!

Long time, no see.

1-d/2-b/3-d

I just read 3-4 lines and already it looks like an awesome article.

Thanks a lot!!!

Mrunal sir,please upload gs pre analysis.

What is the meaning of ‘parent bank” in the statement If the parent banks fail? Please suggest!

A parent bank normally refers to a bank that is in one country(home country) and has subsidiaries in other country. However, I think in this context it refers more to exceptionally important banks from the home country’s perspective. I inferred that from the example given.

Parent bank in given context is that bank which has other subsidiaries and ventures,

e.g- SBI Bank is parent bank for SBI mutual fund and SBI insurance.

thanks sir, and plz keep on posting new articles on various topics …,like basel 3 norms and requirements and more nd topics. it’s of much help. i m deeply indebted to u for your endeavor .

1.D

2 B

3 D

thank you sir,

waiting for your article

Thank you SIr

Hii

anyone preparing for APFC examination?

anyone preparing for APFC examination?